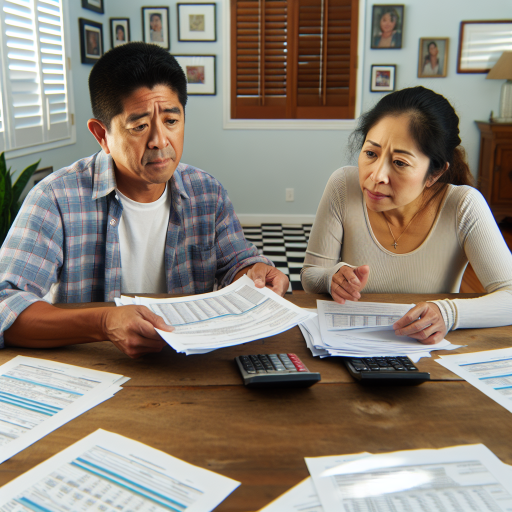

Understanding the Importance of Long-Term Financial Planning as a Homebuyer

Defining Long-Term Costs

Long-term costs encompass various expenses associated with homeownership.

They include mortgage payments, property taxes, and insurance premiums.

Additionally, maintenance, repairs, and utility costs are important considerations.

Being aware of these ongoing expenses can help you budget effectively.

Why Long-Term Financial Planning Matters

Planning for long-term expenses enhances your financial stability.

It prevents unexpected financial burdens in the future.

Moreover, accurate planning helps you avoid financial strain due to unforeseen costs.

Strategies for Effective Long-Term Planning

Begin by creating a comprehensive budget that includes all possible expenses.

Consider setting aside a dedicated emergency fund for unexpected repairs.

In addition, assess potential increases in property taxes and insurance rates.

Consult with a financial advisor to develop a personalized plan.

Prioritizing Savings for Homeownership

Savings should be a key focus in your long-term financial plan.

Allocate a percentage of your income specifically for home-related costs.

Furthermore, explore high-yield savings accounts to maximize your savings growth.

Understanding Market Trends and Housing Costs

Stay informed about local real estate market trends and property values.

Consider how economic conditions may affect your home’s future value.

Being proactive prepares you for potential market fluctuations.

Preparing for Maintenance and Repairs

Regular home maintenance can prevent costly repairs down the road.

Set aside funds specifically for maintenance each month.

Additionally, learn about basic home repairs to save on professional services.

Assessing Your Current Financial Situation

Understanding Your Income

Begin by analyzing your total income sources.

Include your salary, bonuses, and any side incomes.

This helps determine how much you can afford monthly.

Reviewing Your Savings

Next, take stock of your current savings.

Identify funds available for a down payment.

Consider liquid assets that can be quickly accessed.

Determine if you have enough reserves for emergencies.

Evaluating Your Debt

Assess your existing debts, like student loans, credit cards, or car payments.

Calculate your total monthly debt payments.

Compare this amount to your income to evaluate your debt-to-income ratio.

A lower ratio indicates a healthier financial state.

Creating a Budget

Implement a budget to monitor your expenses.

Track discretionary spending vs. essential expenses.

This can help allocate more funds towards savings.

Adjust your lifestyle if necessary to achieve your financial goals.

Setting Financial Goals

Identify specific financial goals to guide your planning.

Consider short-term goals like saving for a down payment.

Also, think about long-term goals such as retirement savings.

Set realistic and measurable objectives to stay on track.

Seeking Professional Advice

Consider consulting with a financial advisor if needed.

An expert can provide tailored advice based on your situation.

This can offer additional insights into your financial health.

Moreover, they might help identify potential investments.

Factors Influencing Long-Term Homeownership Costs

Understanding Taxes

Property taxes significantly impact your overall housing costs.

Local governments assess property values regularly.

Tax rates vary by location, affecting your financial plans.

Research the average tax rates in your desired area.

Consider future property tax increases when budgeting.

Utilizing exemptions and deductions can help reduce costs.

Insurance Considerations

Homeowners insurance protects your investment against damages.

Premiums differ based on location and home value.

Natural disaster risk can increase your insurance costs.

Shop around for the best insurance policy for your needs.

Ask about bundling options for discounts on policies.

Regularly review your coverage to ensure it meets your needs.

Maintenance Expenses

Regular maintenance is essential for long-term homeownership.

Set aside a percentage of your home’s value for upkeep.

Older homes often require more frequent repairs.

Plan for seasonal maintenance tasks, like HVAC checks.

Consider DIY projects to save on labor costs.

Hiring professionals may be necessary for complex tasks.

Utility and Homeowner Association Fees

Utility bills can fluctuate based on usage and seasons.

Average your monthly costs to create a realistic budget.

Homeowner association fees come with community living.

Factor these fees into your monthly homeownership costs.

Understand what the fees cover for better financial planning.

Review any potential future increases in fees.

Find Out More: What To Know About HOA Fees As A First-Time Homebuyer In The USA

The Role of a Mortgage Calculator in Estimating Monthly Payments and Long-Term Costs

Understanding Mortgage Calculators

A mortgage calculator is an essential tool for homebuyers.

It helps you estimate your monthly mortgage payments.

Additionally, it can factor in other costs related to homeownership.

Using a calculator gives a clearer picture of affordability.

This aspect is crucial for first-time buyers in the USA.

How Mortgage Calculators Work

These calculators require specific input from users.

You will need to enter the loan amount you expect to finance.

The interest rate is another critical factor in the calculations.

Other inputs include the loan term and down payment amount.

After entering these details, the calculator provides estimates.

Estimating Monthly Payments

Calculators generate an approximation of your monthly payments.

They typically display principal and interest payments.

Furthermore, they may consider property taxes and insurance costs.

This comprehensive view is beneficial for budgeting effectively.

Long-Term Cost Considerations

Beyond monthly payments, it’s essential to plan for long-term costs.

Mortgage calculators help project total interest paid over the loan’s life.

They can also estimate the impact of property tax increases.

Adjusting the figures can clarify financial responsibilities throughout the loan period.

Benefits of Using a Mortgage Calculator

- It enhances financial planning for potential homeowners.

- The tool allows for adjustments to explore various scenarios.

- Users can see how different interest rates affect overall payments.

- Calculators make it easier to compare different loan offers.

Finding the Right Calculator

There are numerous mortgage calculators available online.

Look for established financial websites to ensure accuracy.

Some banks and credit unions also provide calculators on their platforms.

Using a reputable source gives you reliable estimates.

Ultimately, the right calculator will simplify your homebuying process.

Uncover the Details: Home Inspection Checklist For Identifying Common Seller Repairs

Creating a Comprehensive Budget for Homeownership

Understanding Long-Term Costs

First-time homebuyers should consider various long-term costs when budgeting.

These costs often extend beyond the initial purchase price of the home.

Homeowners often face expenses like property taxes, insurance, and utilities.

Additionally, maintenance costs can vary based on the home’s age and condition.

It is essential to plan for these expenses to avoid financial strain.

Allocating Funds for Repairs and Renovations

Setting aside a specific budget for repairs is crucial for homeowners.

Start by estimating potential repair costs based on the home’s current condition.

Common repairs include roof replacements, plumbing fixes, and electrical updates.

It’s wise to allocate a percentage of your home’s value for yearly maintenance.

Generally, aim for about one to two percent of the home’s value annually.

Creating a Repair and Renovation Plan

Developing a repair and renovation plan helps manage costs effectively.

Begin by making a list of necessary projects and their estimated costs.

Prioritize these projects based on urgency and importance.

Moreover, consider tackling smaller projects first to manage your budget better.

For larger renovations, explore financing options to ease upfront expenses.

Emergency Fund Considerations

An emergency fund for home repairs helps mitigate unexpected costs.

Experts recommend saving at least three to six months’ worth of expenses.

Include funds specifically designated for emergency home repairs in this fund.

Examples include unexpected plumbing issues or sudden roof leaks.

Having this cushion will provide peace of mind for homeowners.

Utilizing Professional Resources

Consulting with professionals can help with budgeting for home ownership.

Home inspectors can provide insights about potential repairs and costs.

Financial advisors can assist in creating sustainable long-term budgets.

Real estate agents often have experience with repair concerns in various neighborhoods.

Utilizing these resources will enhance your planning efforts significantly.

Uncover the Details: Navigating Legal Obligations Through A Comprehensive Home Inspection Checklist

Building an Emergency Fund

Importance of an Emergency Fund

As a new homeowner, budgeting for unexpected costs is crucial.

An emergency fund acts as a financial safety net.

This fund helps cover sudden repairs, maintenance, or emergencies.

Homeownership often comes with unanticipated expenses.

Having funds set aside can reduce stress during tough times.

How Much to Save

Financial experts recommend saving three to six months’ worth of expenses.

Consider your monthly mortgage, utility, and maintenance costs.

This range helps ensure coverage for emergencies.

Assess your unique financial situation to set an appropriate goal.

Building Your Fund

Start small by setting aside manageable amounts each month.

Automate transfers to your emergency fund savings account.

Consistent contributions lead to gradual growth over time.

Tax refunds or bonuses can provide significant boosts.

Use windfalls to contribute more to your fund.

Where to Keep Your Emergency Fund

Choose a high-yield savings account for your emergency fund.

Interest earnings can help your savings grow steadily.

Ensure the account is easily accessible in emergencies.

Check for any fees that might diminish your savings.

Reviewing and Adjusting Your Fund

Regularly review your emergency fund goals and balances.

Consider changes in your lifestyle or expenses that may affect your needs.

Adjust your savings rate accordingly to stay on track.

Evaluate your fund at least once a year for improvements.

Uncover the Details: How To Navigate Real Estate Listings As A First-Time Homebuyer

The Impact of Location on Property Taxes and Utility Costs Over Time

Understanding Property Taxes

Property taxes vary significantly by location across the United States.

Each state has its own tax assessment policies.

Consequently, property taxes can be a major expense for homeowners.

For example, homeowners in New Jersey typically pay higher property taxes.

In contrast, states like Hawaii may have lower rates.

As a first-time homebuyer, it is crucial to research the local tax rates.

Check with the local tax assessor’s office for specific rates.

Utility Costs and Their Variance

Utility costs also fluctuate based on your location.

Regions with extreme climates generally incur higher utility expenses.

For instance, states like Arizona have higher electricity costs in summer.

Conversely, northern states may see increased heating costs in winter.

Research average utility costs in your potential neighborhoods.

Request past utility bills from sellers to estimate future expenses.

Long-Term Budget Considerations

Understanding both property taxes and utility costs helps in long-term budgeting.

First-time buyers should factor these costs into their monthly budget.

Using a budgeting tool can assist in tracking expenses efficiently.

Always include a buffer for unexpected increases in costs.

Furthermore, consider the potential for tax rate changes in the future.

Staying informed about local government policies is crucial.

Planning for Responsible Homeownership

Location significantly impacts property taxes and utility costs.

Being prepared for these expenses can aid in responsible homeownership.

Plan wisely as you embark on your journey as a homeowner.

Exploring First-Time Homebuyer Programs and Grants to Support Long-Term Financial Goals

Understanding Available Programs

First-time homebuyers have various programs to help them succeed.

These programs often include financial support for down payments.

Additionally, many states offer grants specifically for first-time buyers.

Researching these options can save you significant money over time.

Federal Housing Administration Loans

The Federal Housing Administration (FHA) provides accessible loans.

FHA loans allow lower down payments and more flexible credit requirements.

Homebuyers can finance 96.5% of the home with these loans.

Lower closing costs make this an appealing option for many.

USDA Loans

USDA loans are fantastic for rural or suburban homebuyers.

They offer zero down payment options for qualifying borrowers.

These loans come with lower mortgage insurance costs compared to FHA loans.

Eligibility criteria include income limits and property location requirements.

VA Loans for Veterans

Veterans and active military members benefit from VA loans.

These loans do not require a down payment or private mortgage insurance.

Interest rates are often lower than conventional loans.

This makes homeownership more attainable for service members.

State and Local Grants

Many states and local governments offer grants for first-time homebuyers.

These grants can help cover down payments and closing costs.

Eligibility requirements vary, so checking your specific area’s offerings is essential.

Local housing agencies are valuable resources for information.

Tax Credits and Deductions

Some states provide tax credits for first-time homebuyers.

These credits reduce the amount of state income tax owed, saving money.

Moreover, you may qualify for mortgage interest deductions on your federal taxes.

Understanding these benefits is vital for long-term financial planning.

Importance of Budgeting for Long-Term Costs

While securing a home is important, budgeting for ongoing expenses is crucial.

Homeowners should prepare for property taxes, home insurance, and maintenance.

Setting aside funds for these costs will prevent future financial strain.

Consider creating a separate savings account for these ongoing expenses.